What the Bain Global Luxury Report 2026 Actually Proves About the Collapse of Sign-Value and the Rise of the Post-Growth Consumer

When the market's own data confirms what critical theory predicted: the Hollowed Object is not a crisis — it is the new baseline.

The Bain global luxury report 2026 — formally titled Finding a New Longevity for Luxury, produced by Bain & Company in partnership with Altagamma — arrives at a peculiar historical moment. The consultancy frames it as a recovery document: a market that contracted from 400 million active luxury consumers to 330 million between 2022 and 2025 is now poised for a 3- to 5-percent rebound, anchored by the claim that more than 70 percent of lapsed customers say they intend to return within three years. The press received this figure as optimistic. The PLCFA framework reads it as a structural confession.

This study diagnoses the Bain report not as a recovery forecast but as the empirical confirmation of three theses that the Post-Luxury Conceptual Functional Art framework has advanced since OAC's foundational study on Jean Baudrillard's theory of the simulacrum: first, that sign-value — the semiotic engine of the conventional luxury system — has undergone structural collapse rather than cyclical correction; second, that the luxury polycrisis and consumer shifts Bain labels a 'polycrisis' are not disruptions to the system but revelations of its internal contradiction; and third, that the consumer who has exited the personal luxury goods market has not exited the desire for luxury — they have exited the Hollowed Object, and what they seek in its place is precisely what the post-luxury market redefinition cannot supply through price correction and creativity campaigns: meaning over possession. The PLCFA terms active in this study are: Hollowed Object, Sign Value, Zero-Sum Aura, Semantic Burden, Speculative Velocity, Post-Growth Citizen, Atmospheric Equity, and Institutional Necrophagy.

The Recovery Narrative as Ideological Operation

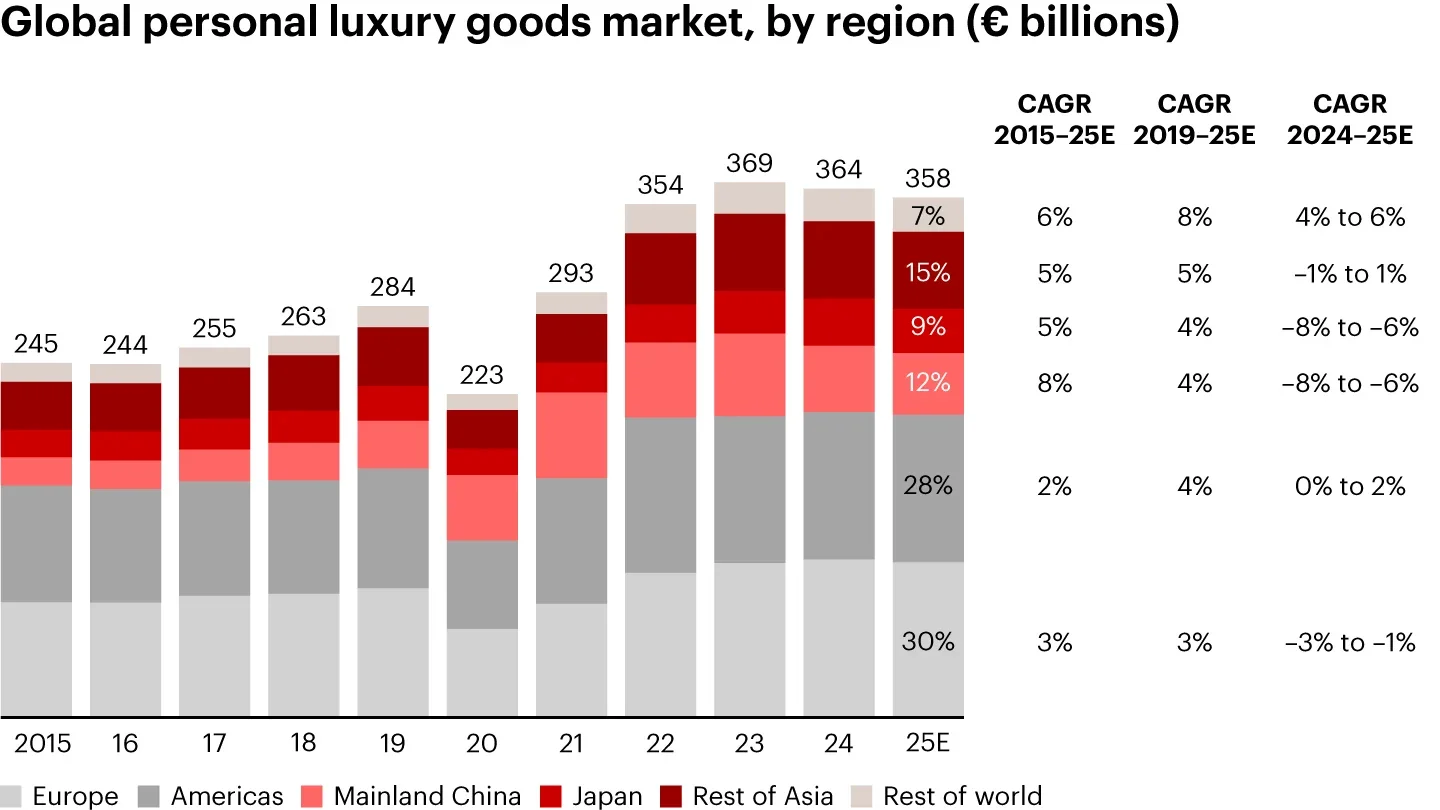

When Bain & Company announced that the personal luxury goods market had contracted from €369 billion in 2023 to €358 billion in 2025 — losing 70 million active consumers over three years — the dominant press coverage sought a reassuring frame. Bloomberg, Reuters, and the Financial Times Business of Luxury Summit all converged on the same narrative architecture: disruption, resilience, rebound. The numbers told a story of temporary dislocation. The consultancy's own language cooperated. Seventy percent of lapsed customers intend to return. Growth of 3 to 5 percent is projected for 2026. The 'polycrisis' is real, but the 'structural fundamentals' remain sound.

The recovery narrative is itself an ideological operation. It requires that the 70-million-consumer exodus be categorized as a disruption — something that happened to the luxury market from outside — rather than as a structural disclosure: the moment when the system's internal contradiction became visible. The sign value economy of conventional luxury depends on a specific relationship between the consumer and the object: the object must carry sufficient semiotic authority — brand heritage, price signal, social legibility — to justify the premium. When that authority erodes, the system does not stutter. It is revealed.

Regional breakdown of the macro contraction, mapping the multi-year decline from the 2023 peak down to €358 billion.

“The 70 percent who say they plan to return are not returning to the object. They are returning to the idea of the object, which is precisely what the Hollowed Object has already consumed.”

Bain's own data contains the evidence. Brand-related searches down by more than 40 percent for more than 40 percent of luxury brands. Social media follower growth collapsed by 90 percent. Engagement rates off by 40 percent. These are not metrics of cyclical demand contraction. These are metrics of semantic burden collapse — the moment at which the object can no longer carry the weight of meaning the consumer placed on it. The consumer did not exit. The object failed.

The empirical metrics of semantic exhaustion: visual proof of the 70-million-consumer mass exodus from the active luxury market.

What 'Polycrisis' Actually Names

Bain's deployment of the term 'polycrisis' — borrowed from geopolitical risk discourse — to describe the overlapping pressures facing luxury in 2025 is revealing precisely because it is a category error. A polycrisis is a condition in which multiple separate crises interact to produce a compound effect greater than the sum of their parts. The term implies that the component crises are, individually, soluble — that the system would be recoverable if any one or two factors were resolved. Tariffs ease, China sentiment recovers, and European consumer confidence firms. In that framing, the luxury market's difficulties are external and conjunctural. They are not.

The luxury polycrisis and consumer shifts Bain catalogs are better understood as the simultaneous rupture of multiple load-bearing fictions of the conventional luxury system. Price elevation was a fiction of value creation — the claim that higher prices signal higher worth rather than extracting rent from captive desire. The creativity deficit is a fiction of cultural authority — the claim that luxury brands operate as cultural producers rather than Hollowed Objects whose cultural content was long since evacuated. Customer base erosion is the collapse of the fiction of inclusivity — the claim that aspirational luxury was democratizing rather than systematically excluding the aspirational consumer to protect margins. None of these are cyclical corrections. All of them are structural revelations.

“A polycrisis is not a collection of problems. It is a system revealing what it always was, and what it could not sustain pretending to be.”

OAC's prior study on the financialization of luxury bags through the LUXUS Fund established the Speculative Velocity thesis: that when objects cease to generate meaning and begin to generate yield, they have completed the conversion from cultural object to financial instrument. The Bain report inadvertently confirms this: the ultra-wealthy consumers who now account for 46 to 47 percent of the personal luxury goods market are not buying luxury as culture. They are buying it as positional collateral. Their spending has plateaued not because they lack capital but because even positional collateral requires some residual cultural authority to perform its function. When the brand's semiotic register is empty, the object cannot serve even as status signal — only as a receipt.

The Speculative Velocity thesis confirmed: ultra-wealthy buyers consolidating control over 46% of total market spend, treating luxury as positional collateral rather than culture.

The Hollowed Object as Market Condition

The central diagnostic contribution of this study is the identification of the Hollowed Object as the defining market condition of the personal luxury goods segment in 2025-2026 — not as a property of individual failed brands but as the systemic state of the category. The Hollowed Object, as developed across the OAC archive — from the foundational Baudrillard study on simulacra to the Paris Fashion Week calendar burnout analysis — describes the object from which the semantic burden has been evacuated: the object that carries the form of meaning without its substance. The Hollowed Object is not a bad product. It is a product that has been de-signified through overproduction, price manipulation, and the replacement of cultural content with marketing content.

Bain's data maps this precisely without naming it. Leather goods and footwear — historically the engines of luxury profitability, the category most dependent on brand-as-sign — contracted sharply under what the report calls 'price sensitivity among aspirational consumers and a perceived lack of creative renewal.' Jewelry, eyewear, and fragrances held firm. The differential is not accidental. Fragrance and jewelry retain a higher phenomenological-to-semiotic ratio — they affect the body directly, independent of brand recognition. Leather goods and footwear, by contrast, are almost entirely semiotic: their value is their legibility as luxury signals. When the signal fails, the object fails.

The Hollowed Object mapped by category: leather goods and footwear contract sharply as purely semiotic signals fail, while higher phenomenological categories like jewelry and beauty hold ground.

“The luxury object is not in crisis because consumers have stopped wanting luxury. It is in crisis because the object stopped being a luxury, and kept its price.”

This is the Zero-Sum Aura dynamic: aura is non-renewable. Once evacuated through overproduction, logo proliferation, and systematized scarcity theater, it cannot be restored by hiring a new creative director or reprinting a heritage campaign. The consumer who left the Brunello Cucinelli cashmere sweater — or chose a Chinese domestic brand offering demonstrable Labor Density at a fraction of the European price — has not made an irrational decision. They have made a post-semiotic decision: I will not pay the sign premium when the sign no longer signifies.

Visualizing the Zero-Sum Aura: soft luxury goods bear the entire brunt of the structural contraction, accounting for over 110% of the market collapse.

The Betrayal Economy and What It Reveals About Desire

Federica Levato, Bain's senior partner leading its EMEA Fashion & Luxury practice and co-author of the report, offered the most significant statement in the entire corpus of Bain's 2025-2026 luxury research: 'You cannot target only the top customers. Because they are also starting to really be upset and to feel betrayed in this industry.' The word 'betrayed' is doing critical work here. Betrayal is not the language of market dynamics. Betrayal is the language of a broken promise — of a relationship that was premised on a claim of mutual value that one party has violated.

The promise luxury made to its consumers — including its ultra-wealthy consumers — was the promise of aura: that the object was genuinely exceptional, genuinely rare, genuinely the product of extraordinary human skill and cultural intelligence. The price was the symbolic contract encoding that promise. When brands raised prices by 40 percent above 2019 levels while delivering creative output that the market's own engagement metrics rated as in decline, they did not merely disappoint consumers. They voided the contract. The consumer was not responding to economic pressure. They were responding to a trust crisis — the recognition that the promise was never backed by the substance it claimed.

This analysis intersects with OAC's research on the Miu Miu viral moment and the post-aspirational consumer, which established that the existing consumer is not simply price-sensitive — they are semantically exhausted. They have processed the luxury sign system to saturation and found it empty. Bain's data on accessible luxury brands' relative outperformance during the same period in which heritage houses contracted confirms this reading: consumers are not abandoning luxury as a category. They are abandoning luxury as a semiotic system whose signs have been devalued by the very brands that issued them.

“Betrayal implies that the consumer believed the promise. The crisis is not that they stopped believing. It is that the brands stopped earning the belief.”

The Betrayal Economy in numbers: aspirational consumers reject the empty price hikes of legacy heritage houses, leading to a 75% negative revenue growth polarization among aspirational brands.

The Post-Growth Consumer: What the 70 Percent Actually Signal

The figure that received the most optimistic interpretation in the financial press deserves the most rigorous reinterpretation: more than 70 percent of lapsed luxury customers indicate they intend to resume purchasing within three years. Bain presents this as evidence of durable demand, a structural reserve of desire that will flow back into the market as conditions improve. The post-luxury market redefinition framework reads it differently. The 70 percent are not waiting for prices to drop or creativity to improve. They are waiting for luxury to become worth the custodian's contract again — the implicit agreement that the object will carry meaning across time, that it will become more over its life rather than depreciate as a sign.

This is the Post-Growth Citizen as consumer: not the degrowth ascetic who rejects luxury on principle, but the consumer who has evolved beyond the sign-value economy into a desire for meaning over possession. They still want what luxury used to be able to give: the encounter with human mastery, the object that accrues rather than depreciates, the thing that positions them not in a social hierarchy but in a relationship with time and craft. What they refuse to pay for is the Hollowed Object wearing luxury's credentials without luxury's substance.

Bain's own prescription for recovery confirms this reading without theorizing it: brands must 'reestablish creativity, quality, and purpose as non-negotiable pillars.' The language of purpose is the consultancy's accessible translation of what the PLCFA framework calls narrative permanence: the object's capacity to carry a coherent story of its own making — material, maker, intention, and consequence — that exceeds the transaction and survives it. The 70 percent are not a market waiting to return. They are the advanced signal of a consumer type for whom conventional luxury no longer exists in sufficient supply.

“The 70 percent are not a recovery cohort. They are the post-luxury consumer-in-waiting, and the conventional luxury market cannot build what they are waiting for.”

Emotive Branding as Category Error

The Bain report's prescription for recovery centers on what it calls a 'redefinition of value and meaning' — a pivot toward what its analysis identifies as the primary driver of market growth: experiences and emotions. The report's EMEA practice lead describes the transformation underway as one in which 'experiences and emotions become the primary driver of market growth after the shopping-spree era.' Gourmet dining, wellness, elite sports, travel experiences — the Bain analysis identifies these as the new luxury, the areas where consumers are spending the budget previously directed at leather goods and shoes.

This observation is empirically accurate. The diagnosis it implies, however, is a category error. The conventional luxury system's response to the shift toward experience has been emotive branding in the luxury market: the injection of emotional content into object marketing, and the deployment of storytelling as a substitute for the authentic Labor Density and narrative permanence that the consumer actually seeks. Emotional content produced by marketing departments is not equivalent to emotional content produced by the object's own making. The consumer — particularly the post-growth citizen who has processed the luxury sign system most thoroughly — distinguishes between the two.

The OAC study on Bank of America and ArtTactic's market analysis established the anti-speculative autonomy principle: that the object which refuses to perform emotiveness is more emotionally authoritative than the object designed to communicate feeling. The Atmospheric Equity of genuinely labor-dense, materially singular work is not reproducible through campaign investment. It is produced through the work itself, which is why the conventional luxury system, having dismantled the conditions of that work in pursuit of a scalable margin, cannot simply restore it through marketing.

“Emotive branding is the system’s attempt to buy back the feeling it sold off. It cannot. Feeling is not a brand asset. It is a material consequence.”

Institutional Necrophagy: What 'Longevity' Actually Means

The title of the Bain report — Finding a New Longevity for Luxury — is the most philosophically revealing element of the entire document. Longevity is not a business metric. It is a temporal claim: the assertion that the object, the brand, or the institution has a relationship with time that extends beyond the transaction cycle. The framing implicitly acknowledges that the existing relationship with time has been severed. The industry does not need new longevity. It destroyed the longevity it had and is now attempting to reconstitute it from the outside — from consultancy prescriptions, campaign pivots, and creative director appointments.

This is what the PLCFA framework diagnoses as Institutional Necrophagy: the feeding of a living institution on the cultural capital of its own dead history. The heritage campaigns that dominate luxury marketing in contraction periods are not acts of cultural recovery. They are acts of cultural extraction — the deployment of accumulated semiotic capital as a substitute for its current production. Heritage is spent, not stored. Every invocation of archive without present creative substance accelerates the Zero-Sum Aura dynamic: the total available aura diminishes while the demand on that aura increases.

The Bain report notes that brand-related searches are down for more than 40 percent of luxury brands, even as those brands have increased archive mining and heritage storytelling. This is not a correlation. This is the necrophagic mechanism: the more the brand feeds on its past, the more the consumer registers the absence of its present. The consumer who searches for a brand and finds only a retrospective narrative is confirming that the brand has converted from a cultural producer to a cultural museum, and museums, as the PLCFA study on dark mode auction practices established, are not where desire is generated.

“Longevity is not a strategy. It is a consequence of making things that matter, in ways that hold, for reasons that survive the transaction.”

The PLCFA Position: What the Report Cannot Say

The Bain report cannot say what it confirms because saying it would require the dissolution of its client base. The consultancy's prescription — 'reestablish creativity, quality, and purpose' — is structurally incapable of reaching its stated conclusion because it cannot recommend abolishing the production conditions that gave rise to the crisis. Scalable luxury production, licensing-dependent margin, and celebrity brand endorsement are not incidental to the Hollowed Object — they are its manufacturing process. The recommendations leave these conditions intact and propose that creativity and storytelling, deployed atop them, will restore the aura they have consumed.

The PLCFA framework occupies the position that the report cannot. The One Original Principle — one work, one maker, one custodian, no editions, no multiples — is not a boutique affectation. It is the structural antithesis of every condition that gave rise to the luxury polycrisis. The Custodian's Contract is not a marketing narrative about stewardship. It is a legal and ethical structure that makes scalability impossible and mandatory. The Material Singularity principle is not a design aesthetic. It is the insistence that the object's physical substance carry its full moral and historical weight, which requires that the weight be genuine, which requires that the production conditions produce genuine weight, which is irreconcilable with the conditions that produced the polycrisis.

This is not a critique of Bain & Company, which is doing what consultancies do: providing actionable prescriptions within the constraints of the existing system. It is a structural observation: the prescriptions are bounded by the system they serve. The post-luxury market redefinition that Bain's data points toward is not achievable within the conventional luxury system. It requires the construction of an alternative, which is what the Objects of Affection Collection has built, and what 70 percent of lapsed consumers are waiting, without knowing it, to find.

“The report confirms the diagnosis. It cannot recommend the cure because it requires dismantling the patient.”

K-Shaped Luxury and the Atmospheric Equity Gap

The Bain report's identification of 'K-shaped' luxury dynamics — ultra-wealthy buyers sustaining demand at the high end while aspirational consumers withdraw — maps precisely onto the K-Shaped Luxury and Atmospheric Equity theses developed in prior OAC market studies. The K-shape is not merely a distribution of spending. It is a distribution of access to meaning: the ultra-wealthy retain access to the genuinely scarce, the genuinely made, the genuinely rare — if they seek it — while the aspirational consumer is offered manufactured scarcity and legacy brand equity at prices that no longer correspond to genuine making.

The Atmospheric Equity gap is the difference between the object's claimed atmosphere — the density of human intention, skill, and cultural intelligence it presents as its value proposition — and the actual atmosphere it contains. In a high-Atmospheric-Equity object, the gap is zero: what the object claims, it delivers. The Hollowed Object is defined by a large and growing gap: the atmosphere is entirely claimed, none of it is delivered. The K-shape is the market's spatial expression of this gap: those who can afford to close it by accessing truly rare objects at any price do so; those who cannot afford that tier encounter only the gap, and withdraw.

The Atmospheric Equity Gap visualized: consumers bypass modern retail margins entirely, driving the secondhand market index to 249 as they seek historical substance over new, manufactured scarcity.

The Bain prescription for restoring the aspirational consumer — 'reestablish creativity, quality, and purpose' — implicitly acknowledges the Atmospheric Equity gap without naming it. The problem is that creativity, quality, and purpose at scale require the same industrial conditions that produced the gap. The brands that contracted the most sharply — the leather goods and footwear categories — are precisely the categories most dependent on scaled production and most exposed when the gap between claimed and actual atmosphere is interrogated by a consumer who has stopped performing credulity.

What the Report Leaves Structurally Open

The Bain Global Luxury Report 2026 confirms three things that the PLCFA framework has held since OAC's foundational studies on simulacra and sign value collapse: that the Hollowed Object is not a brand failure but a category condition; that the exiting consumer is not an economic casualty but a post-semiotic agent seeking meaning over possession; and that the conventional luxury system's prescription for its own recovery — more creativity, more purpose, more storytelling — is bounded by the very production conditions that evacuated the meaning in the first place.

What the report leaves structurally open is the space the PLCFA framework occupies: the construction of an object-world in which the Atmospheric Equity gap is structurally impossible because the production conditions do not permit it. The One Original Principle, the Custodian's Contract, the Material Singularity imperative — these are not alternatives to the luxury system. They are the conditions under which an object can again carry the semantic burden the consumer has always demanded and the conventional system has systematically failed to supply.

The 70 percent waiting to return are not a recovery market. They are the confirmation that desire remains — that the post-growth citizen has not abandoned the object but upgraded the demand. What they are waiting for cannot be built from a Bain prescription. It has to be built from first principles — from labor density that is actual, from narrative permanence that is earned, from atmospheric equity that is structural. The report confirms the crisis. The PLCFA framework is the architecture of its resolution.

Authored by Christopher Banks, Anthropologist of Luxury, Critical Theorist & Founder

Objects of Affection Collection

Office of Critical Theory & Curatorial Strategy

469 Fashion Avenue, 12th Floor, New York, NY 10018RELATED OAC STUDIES

Expand the archive. Each study below deepens one dimension of the argument above.

Sign-Value Theory & The Simulacrum

· The Banksy Enigma: Mastering the Narrative of Modern Art

· The New Avant-Garde: Deconstructing Status and Utility in the Age of Post-Luxury

Market Collapse & Financialization

· The Miu Miu Problem: How Wisdom Kaye's Viral Meltdown Became a Blueprint for a New Philosophy

· The Art of Being: A Guide to a Life of Cultivated Grace

Post-Growth Consumer & Quiet Luxury

· The Modern Tailor as a Cultural Synthesizer: Charlie Casely-Hayford

· The Art of Being: A Guide to a Life of Cultivated Grace

Material Singularity & Labor Density

· The Forging of a Legend: Goro's, A Philosophy Embodied in Silver and Gold

· The Fluidity of Form: How Iris van Herpen is Rewriting the DNA of Haute Couture

· Hiroshi Fujiwara and the Architecture of Post-Luxury Influence